Irish Banking in a digital age

Index

Introduction

Case Study

- Information Systems used by NTUC Income before Migrating

- Business Processes used by NTUC Income before Migrating

- Problems Associated with the Old Systems

- New Digital System capabilities

- How did the new system resolve the problems

- How did the new digital system provide a basis for the orange strategy

- Could Orange have been available with the Old systems

- Three Important Lessons for Irish Retail Banking

Conclusion

Introduction

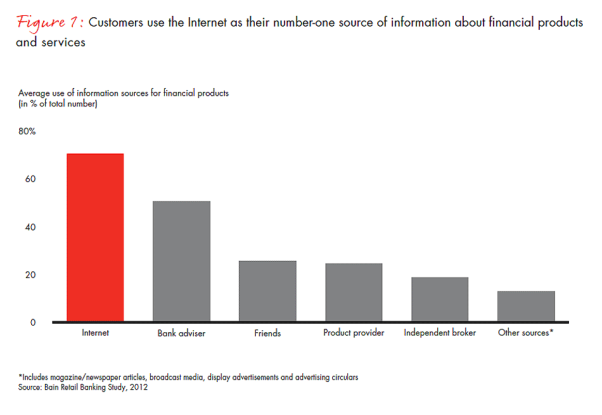

Banking in a digital age is a huge subject and I have gone into some detail to analyse the case study and to answer the questions outlined. However I want to initially highlight the diagrams below, the first diagram shows the percentage of customers that consult the internet and is self-explanatory, however it does highlight how important the internet is to banks to create revenue and to ensure their viability on into the future. The second diagram however is somewhat of a parallel to this in that it shows that younger customers are inclined to bank with larger well known banks regardless. An interesting argument could be given for both sides.

Case Study

- Information systems used by NTUC Income before migrating were:

- Old fashioned HP 3000 mainframe system

- Decades old Cobol programs

- Batch processing systems,

- Agents tried to submit the documents using notebooks

- Business Processes Used by NTUC Income before migrating to new digital systems were:

- Entirely paper based

- Customers met with broker/agent to complete proposal form

- Form is submitted by courier to Office service department

- Form is logged and sorted

- Form is then sent to underwriters.

- Accepted proposals then sent to computer Services Department be printed and distributed.

- All original documents then sent to storage unit for logging and filing

- In a lot of cases departments had to pass physical documents among each other

- Problems Associated with the Old Systems

- Very cumbersome and time consuming process

- After proposal form completed by customer it could take 2 to 3 days for the form to be couriered to underwriters

- Form then sent to computer services department to be printed and distributed.

- Sent to storage unit to be logged and stored which could take over two to three days

- Document retrieval slow and cumbersome taking up to two days to locate, then the form had to be shipped by courier.

- Refiling would take 2 days.

- Documents had to be physically passed to each other

- High volume of staff involved in clerical roles, from start to finish the policy will have been handled by up to 13 staff

- Entirely paper based system

- Existing computer system very unreliable with regular breakdowns

- Breakdowns meant loss of man hours re-inputting lost data

- Existing system had to be backed up daily however if system crashed during the day staff had to choose whether to save daily reconciliation or whether to do a full back up

- If daily back up not completed previous days data would be lost

- No Real time data, systems did not allow data inputter to see if customer is existing or new.

- Loss in revenue and sales due to lack of real time data.

- Existing system had 3 major hardware failures which mean loss of 6 days.

- Regular breakdowns

- No up to date information for departments or internal digital mailing system.

2.1 New digital system capabilities

- New Java based EBao Lifesystem

- All branches equipped with scanners and new monitors

- New PC RAM of 128MB

- New hardware and software for application servers

- Disk storage systems

- Data transmitted immediately

- All Documents scanned and stored on digital devices

- Data stored on two or more servers all connected by two or more connection lines.

- Faster cable

- Wireless capability

- Fiber-optic Backbone

2.2 How did the new system resolve the problems?

– Reduced timeframe for induction of policy

– Efficient scanning and processing systems.

– Real time data, enabling cross sales and cross referencing for existing customers

– Reduction in time to react to market trends and changes.

– Easier to design and launch new products to keep ahead of market trends

– Good backup systems, data saved on two or more servers ensuring no loss of data

– New disaster recovery site that no longer required restoration of the previous day’s data

– Improved customer service as new system gave a single view of each customer showing all real time data allowing cross selling and reduced turnaround times

– Up to 50 percent saving on time and costs

3.1 How did the new digital system provide a basis for the orange strategy?

Orange was stuck in a paper based timewarp. This meant that all time and energy was put into manual applications which did not leave time for them to focus on a more customer friendly and customer focused organization. The new system meant that there was a huge reduction in the need for large volumes of clerical staff and these staff could be utilized to provide a better customer service and also provide a better profit for the business by utilizing the customer information to enable cross sales.

It also enabled time for the marketing strategy to be overhauled as up to date data was now at hand. This data provided a customer profile facilitating the sale of more relevant products by providing some Golden Nuggets of information. As the systems could provide some analytical and operational CRM data.

It also enabled the business to be able to react quickly to any new market trends as the new digital systems were able to take on and launch new products quickly and in fact enabled them to set up a brand new concept in the insurance business, the launch of the Orange motorcycles fleet. This fleet was very distinctive and easily spotted on the high street which in itself was a major marketing tool but they not only serviced their own customers who had accidents but also non customers which in turn meant that these people would go to Orange the next time they needed a quote for insurance and also created a Feel Good moment.

It enabled them to launch Orange Eye which was a smartphone application. This provided an in car camera which helped combat motor insurance fraud which ensured that costs for the company would be kept down and in turn allowed for reduced insurance policies.

3.2 Could Orange have been available with the Old Systems?

Orange would most definitely not have been possible with the old system. They were not able to provide an efficient, straightforward, transparent system or product due to the major constraints of the old systems.

4. Three important Lessons for Irish Retail Banking

1. Banks have to embrace the Digital Age to Increase profit.

Banks have to embrace and utilize all systems available and even create new systems in order to increase revenue and in turn increase profit. According the statistics provided by The Second UPC Report on Irelands Digital future the projected value of the Irish internet economy in 2020 will be E21.1 BN, Projected on line Consumer Spending will be E12.7 BN as opposed to figures provided for 2014 when online consumer spending was E5.9 BN.

Therefore this market has to be tapped to ensure the viability of the bank into the future.

While initially consumers were reluctant to take on some of these new online systems such as online banking one would wonder what their reaction would be if it were to be taken away from them overnight.

As can be seen from table below sourced from PWC the percentage of users of online services has increased tenfold and banks have to embrace this change and utilize it to their advantage.

Gen Y = born 1980, Gen X = born 1965 – 1979, Baby boomers = 1946 – 1964, Matures born prior to 1946

2. Digital systems improve services.

The new orange system allowed for funds and also staff to be freed up to create a much better customer experience. One way of doing this was to send out the Orange Fleet which proved a huge success. This model has been in some way reproduced with banks now beginning to think outside the box, by providing some time/space shifting services such as Mobile Mortgage Managers who will visit you out of bank hours and in turn the new systems that allow you to bank on line 24 hours a day online in the comfort of your own home.

Bank of Ireland are currently trying to promote an internal scoring card system that they call NPS to ensure that we continue to provide an excellent customer service and allowing all opportunities to be utilized and all cross sales achieved to ensure a good profit and also a good service to the customer. As outlined in our lectures 50 percent of time and effort is invested in trying to get new customers in the first place and 50 percent to hold onto them. It costs six times more to get a new customer therefore a high retention of existing customers ensures an increased profit.

Accenture created a Consumer research of over 13000 in 33 countries and they found that 61% if customers globally switched providers due to a bad experience and 85% switch providers because they feel that companies don’t make it easy to do business with.

It is no secret that the general public’s perception of the Banks in light of the recent recession and bailout by the government has not been advantageous and therefore it is in our best interest to improve our systems and also do things a bit differently and this NPS scorecard is in some way helping this.

Also the public would not have great trust in the Banks and again the “simple honest and different approach” adapted by Orange could be adapted in a more robust platform by the Banks.

3. Correct systems have to be in place in order for customers to adapt and embrace the change.

Bank of Irelands digital systems were sometimes seen as cumbersome by both staff and by customers alike. There were some major issues with Banking on line for business customers as it was difficult to get set up and in a lot of cases it wasn’t compatible with certain computer systems.

There is also the public’s perception of the risk concerned with digital technology and some customers do not trust the systems and still prefer to go in to the Bank and make their transactions or apply for their loans with a human. I showed a family member how to pay a bill on line. This was their first attempt at using this system and they were very impressed with how easy the process was, however as the payee was an Ulster Bank customer the transaction took a couple of days to go through. This caused my relation a huge worry (they are in their 60’s) as she would have preferred to have had physical evidence such as a receipt for the transaction and they could not relax until the funds were acknowledged as received. This however is not such a worry for younger generations as they have more trust in the digital systems. The security issues need to be addressed and maintained and also the banks need to keep ahead of the fraudsters. As long as this continues to happen I can see a continued rise in the use of digital banking systems.

Conclusion

As outlined on the Bain Brief article “Many banks have been too quick to capitalize on digital technologies as a way to strip costs out of their operations. Steering their technology-enable customers to websites, mobile apps and ATMs, they are shuttering full-service branches and replacing them with automated kiosks. But while the savings from taking a self-service approach can be enticing, the longer term costs of abandoning customers to their own high-tech devices are unacceptably high.” The Digital Challenge to Retail banks Oct 17,2012 by Dirk Vater, Youngsuh Cho and Peter Sidebottom.

This article was written in 2012 and since then Bank of Ireland has come to realize this and are trying to keep their physical branch footprint in place in as much as possible in order to have a face behind the bank. Other major banks in Ireland have been reducing their branch footprint in order to reduce costs. We will have to wait and see in the future what the best approach to this will have been and as always hindsight is sometimes a great thing.

Referencing

Accenture Study, Global Consumer Pulse Research (2014)

Bain Banking Study (2012)

FIS Primary Consumer Research (Aug 2011)

Laudon, Laudon,(2014) Management Information Systems

Second UPC Report on Irelands Digital Future (2014)

Stapleton, (2015) Banking in a Digital Age Webinars

Putnam, (2011) Attracting and Retaining Gen Y and Gen X

Vater, Youngsuh and Sidebottom (2012) Bain Brief The Digital Challenge to Retail Banks

Villers, (2015) PWC Banking will mean digital banking in 2015

Order Now