Quantitative Easing within the Eurozone

Â

Inflation is one of those things where the situation determines whether it is good or bad. Central Banks (CB’s) are able to steer the inflation rate. Before the financial crisis of ’08-’09, they managed them by interest rate adjustment. The interest rate at which a bank borrows overnight would be reduced to prevent an economic fall, or increased if spending and credit would get out of hand (The Economist, 2015).

When the CB’s lowered their overnight interest rates during the financial crisis, even cutting the rates to almost zero did not manage to cause an economic recovery. Therefore, CB’s started to experiment with alternative methods to encourage banks to pump money in the economy. Quantitative Easing (QE) is one of those alternative tools (The Economist, 2015). The current president of the European Central Bank (ECB), Mario Draghi, announced in January 2015 that he was going to employ QE within the Eurozone (Stewart, 2015).

QE is an unconventional method in which a CB creates money and buys financial assets, such as bonds (Bank of England, n.d.). The use of QE has been popular since the financial crisis. In Europe, the ECB stated in 2009 that they would focus on buying a form of corporate debt, covered bonds, with an initial value of €60bn (Duncan, 2009). In 2015 this eventually became €60bn/month of bonds which would be bought from European institutions, agencies and central governments (Stewart, 2015). In 2016 they also included corporate bonds under their QE program.

QE advantages

In the recent crises interest rates had already been reduced to sub-zero levels, when there was still a need to prevent an economic downturn. Therefore CB’s had no probable course of action anymore. With QE however, CB’s could still influence the economy. QE increases the money supply, which causes competition between lenders due to excess money and therefore lower interest rates. This means that the CB’s do not have to lower the interest rates, as they will automatically go down.

QE also limits the increase in unemployment as result of a crisis, since it prevents in short-term a huge economic fall. The fact that QE shows immediate results, can be used to buy and therefore remove toxic assets, and that the government is in control of the outcomes, make it an interesting alternative to the classic conventional method. With QE CB’s know the exact amount of money that they are implementing in the marketplace (MSG, 2017).

QE disadvantages

One of the CB’s its main tasks is to monitor and control inflation. The inflation target in the EU is just under 2% (European Central Bank, 2017). QE causes a high inflation, due to the fact that money is created to buy the bonds. In the short-term a rise in inflation is a good thing, since shows economic improvement. In the long-term; however, high inflation is a problem. There is no long term data available since QE is a recent phenomenon, but it is a possibility that it could create long term inflation problems (Management Study Guide, 2017).

QE also causes fluctuation in the interest rates, since the higher inflation over time will also make the interest rates rise. This is against the goal of the CB to keep them at a stable level. QE gives improvements in the economy in the short-term, however; in the long-term it could destabilize the economy (Management Study Guide, 2017).

ECB’s decision to choose QE

In June of 2014, the ECB lowered their interest rates to a negative number (CÅ“uré, 2016). The method to decrease interest rates was therefore not really implementable anymore. The ECB had to search for an alternative method to influence the economy. Other CB’s were using QE, and there was also an example where QE had worked (UK, 2009). The need to increase spending combined with the other possible motives could be the reason which pushed the ECB towards QE.

The question now is where the need to increase spending came from. The core of the problems in the Eurozone is a spending crisis. “One person’s spending is another person’s income.” – John Maynard Keynes. In the aftermath of the ’08 crisis, too much debt and poor growth prospects sacrificed spending in the private sector. New banking regulations combined with oversized balance sheets caused unwillingness to expand lending in banks. This combined resulted in dramatic decreases in private sector spending (van Lerven, 2016).

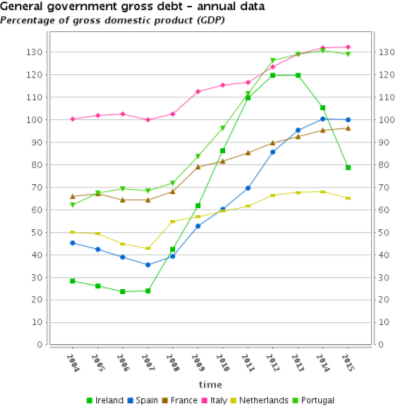

Graph 1

Due to the recession government its social security expenditures increased after they had bailed out banks. The decrease in spending mentioned above meant less tax revenue. These two events combined caused an expansion in government budget deficits, as is clearly visible in the graph above (Eurostat, 2017). This meant that governments also started to cut in their spending, which resulted in lower incomes for households, and therefore lower goods and services demands (van Lerven, 2016).

To be able to give a recommendation to Mario Draghi, it is important to look at the results of their QE program are so far. In the first three months, there was a small increase in prices. However, in the following five months the inflation rate declined progressively and even reached a negative number in September 2015. After this it shows a few rises and falls, but all nowhere near the goal the ECB wanted to achieve with QE (van Lerven, 2016). The inflation was far from just under two percent.

However, there is no long term information available, and QE has worked before. Currently QE aims to stimulate spending indirectly. The ECB does not give money to governments or the normal people, but puts it into financial markets. They then hope that the private sector changes their behaviour when it comes to borrowing and spending. The unfortunate truth is however, that investigation shows that QE has weak results in the transmissions in which it is supposed to work. Assets prices have increased, but there is no noticeable increase in spending in the Eurozone. The results the ECB wanted have not been achieved (van Lerven, 2016).

Recommendation

The current QE program has been here for a couple of years now, and with significant size. The goals the ECB hoped to achieve were not achieved, and therefore it is unlikely that increasing the length or size will lead to the spending they desperately want. As member of the board of governors I would suggest the use of more direct ways to increase the spending in the economy.

Â

Bank of England, n.d. What is quantitative easing?. [Online]

Available at: http://www.bankofengland.co.uk/monetarypolicy/pages/qe/default.aspx

[Accessed 15 February 2017].

CÅ“uré, B., 2016. Assessing the implications of negative interest rates. [Online]

Available at: https://www.ecb.europa.eu/press/key/date/2016/html/sp160728.en.html

[Accessed 28 February 2017].

Coy, P., 2014. Why John Maynard Keynes is just the economist we need to get the world’s economy humming again. [Online]

Available at: https://www.bloomberg.com/news/articles/2014-10-30/why-john-maynard-keyness-theories-can-fix-the-world-economy

[Accessed 28 February 2017].

Duncan, G., 2009. ECB opts for quantitative easing to lift the eurozone. The Times, 8 May, p. 53.

European Central Bank, 2017. Monetary Policy. [Online]

Available at: https://www.ecb.europa.eu/mopo/html/index.en.html

[Accessed 23 February 2017].

Eurostat, 2017. General Government gross debt – annual data. [Art] (Eurostat).

Management Study Guide, 2017. Disadvantages of Quantitative Easing. [Online]

Available at: https://www.managementstudyguide.com/disadvantages-of-quantitative-easing.htm

[Accessed 28 February 2017].

MSG, 2017. Advantages of Quantitative Easing. [Online]

Available at: https://www.managementstudyguide.com/advantages-of-quantitative-easing.htm

[Accessed 28 February 2017].

Stewart, H., 2015. ECB unveils €1.1tn QE plan to stimulate eurozone economy. [Online]

Available at: https://www.theguardian.com/business/2015/jan/22/ecb-unveils-1-trillion-qe-plan-stimulate-eurozoen-economy

[Accessed 12 February 2017].

The Economist, 2015. What is quantitative easing?. [Online]

Available at: http://www.economist.com/blogs/economist-explains/2015/03/economist-explains-5

[Accessed 23 February 2017].

TransferWise Ltd., 2015. What Is Quantitative Easing And Why Is It Used?. [Online]

Available at: https://transferwise.com/gb/blog/what-is-quantitative-easing-why-is-it-used

[Accessed 28 February 2017].

van Lerven, F., 2016. Quantitative Easing in the Eurozone: a One-Year Assessment. Intereconomics, 51(4), pp. 237-242.

Zewald, S. B. J., 2017. Euro’s op tafel gevallen. [Art] (University of Bradford).

Zewald, S. B. J., 2017. Money Printing. [Art] (University of Bradford).

(Zewald, 2017)

(Zewald, 2017)

(TransferWise Ltd., 2015)

(Coy, 2014)

(Eurostat, 2017)